The Rise, Fall, and Rise (and Fall…?) of Cell and Gene Therapy

Carl Schoellhammer, partner, DeciBio

More than $14 billion in announced acquisition value has flowed into in vivo cell therapy companies over the last 18 months. Lilly acquired Kelonia, AbbVie bought Capstan, BMS acquired Orbital, and AstraZeneca bought EsoBiotec, to name a few.

These acquisitions demonstrate that we’re getting closer to the day when single injections that reprogram cells can fight disease without complex shipping logistics, waiting times and toxic preconditioning regimens of first-generation ex vivo cell therapies.

Over the last decade, the cell therapy field has experienced extraordinary breakthroughs and painful corrections. And yet, just as it has emerged from its first major boom-and-bust cycle with hard-won discipline, in vivo cell therapy is generating the kind of excitement that should, by now, feel familiar.

The first modern wave of cell and gene therapy was built on scientific breakthroughs. CAR-T therapies demonstrated that living medicines could deliver long-lasting remissions for cancer patients who were facing a death sentence. Early AAV therapies showed that a single treatment could meaningfully alter the course of genetic disease. It was heady stuff. Investors responded accordingly.

During the pandemic-era biotech boom, capital flooded the sector in search for the next company like Moderna, with a platform technology with broad potential for multiple diseases, like messenger RNA vaccines. Every company seemed to need a cell and gene therapy strategy.

Looking across DeciBio’s TheraTrack database, there was a period where the average indication being addressed (across oncology, rare disease) attracted more than four gene therapy assets and more than 10 cell therapy assets in development. Multiple companies chased the same diseases with limited differentiation. Capital poured in faster than market realities could justify, and scientific possibility increasingly became confused with commercial inevitability.

The sector delivered effective, generally durable treatments, not the one-and-done “cures” the market was promised. The resulting correction was severe, but necessary.

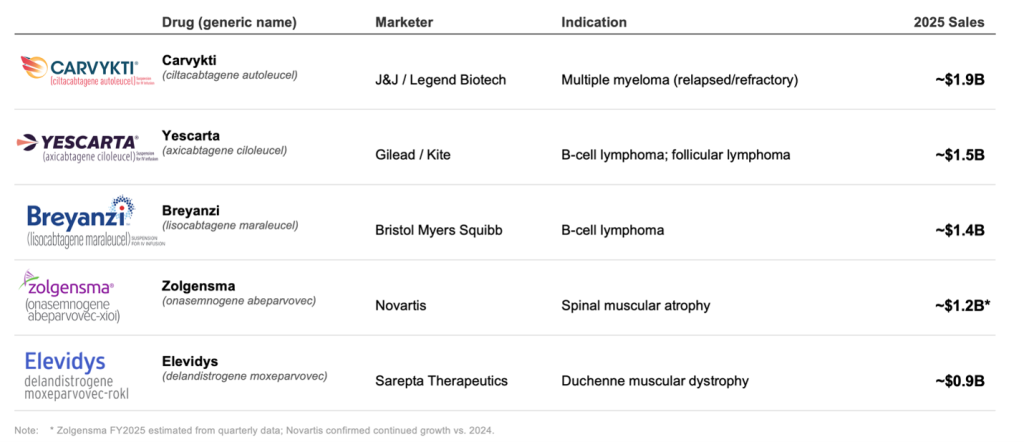

Today, several approved cell and gene therapy products have reached blockbuster status (Table 1). Sectors written off by some investors as dead in 2022 have steadily continued to attract smaller, but still meaningful investments and generate significant transaction value (Figure 1). The manufacturing challenges that once seemed existential are being converted, steadily, from scientific uncertainties into engineering problems.

The correction hurt. It also forced companies to step up their game.

Table 1: Blockbuster cell and gene therapy products

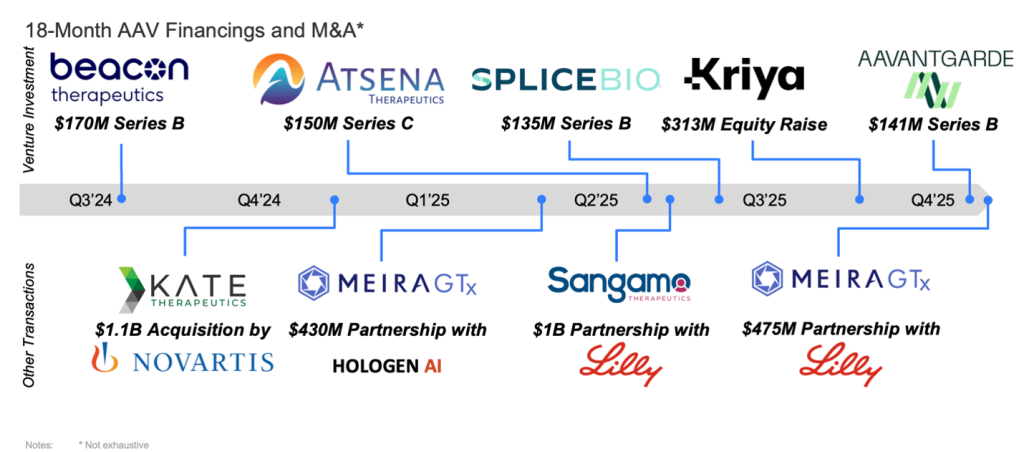

Figure 1: Investment and financings into AAV-based biotech companies

Which brings us to today’s newest source of excitement: in vivo cell therapy. Rather than extracting cells from a patient, engineering them in a manufacturing facility, and reinfusing them weeks later, why not engineer those cells directly inside the body? In theory, this approach could simplify treatment, reduce costs, shorten timelines, and dramatically expand access.

Many of today’s talking points from companies echo the promises made during the first cell and gene therapy boom. Manufacturing will be simplified, costs will fall, and platform technologies will unlock dozens of indications. Investors and companies have flocked to the sector. But who is left to buy the next wave of companies?

The most logical strategic buyers have largely committed. That leaves a meaningfully thinner pool of potential acquirers for the companies now raising capital, building platforms, and conducting early-stage trials. Exit paths matter, and the number of natural buyers for the next cohort may be more limited than the current pace of investment implies.

Manufacturing Challenges Ahead

One of the most common narratives surrounding in vivo cell therapy is that it eliminates manufacturing complexity. It is more complicated than that. In many cases, we may simply be trading one manufacturing challenge for another.

Consider a targeted LNP-based system. Production involves at least three distinct steps, each requiring purification and each introducing yield losses: synthesis of the mRNA cargo, formulation and encapsulation within the lipid nanoparticle, and conjugation of the targeting ligand to the LNP surface. Losses compound at every stage.

Beyond yield, the chemistry itself is not trivial. Conjugating antibodies or peptides to lipid nanoparticle surfaces introduces questions around conjugation efficiency, batch-to-batch consistency, and analytical characterization that the field is still working through.

Then there is the CDMO problem. Targeted LNP products sit at the intersection of lipid chemistry, biologics manufacturing, nanoparticle formulation, and conjugation science. While each capability exists independently, relatively few organizations have deep expertise across all of them within a single integrated process. As these programs scale, developers will need to navigate manufacturing execution and increasingly complex analytical, comparability, and regulatory expectations.

Longer Term Questions

Clinical reality will also eventually arrive. As programs move into larger patient populations and longer follow-up periods, new questions will emerge around safety, durability, repeat dosing, and immune responses.

Cell and gene therapy has never been a story of failure. It has been a story of overestimation followed, more quietly, by real progress.

The danger today is that we once again mistake early promise for inevitability. If the field applies the lessons learned from AAV and CAR-T, the next decade could be transformative. If not, we may simply be boarding the next rollercoaster before the last one has finished its climb.