How the US Can Continue to Lead As China Rises

David Li, co-founder and CEO, Meliora Therapeutics

China made its intentions known 10 years ago. In the “Made in China 2025” plan, released in 2015, the government identified biopharmaceuticals as one of the industries where it sought a world leadership position.

The investment has paid off. By making biotech a top priority, the China biotech ecosystem is now thriving.

As we enter 2025, the strength of China’s biotech industry is evident. Across all modalities of therapeutics, but especially antibodies, T-cell engagers, ADCs, and small molecules, Chinese assets and companies are now competitive for leading the industry.

A foundation for its ascendant life sciences industry has been its R&D productivity, which has quickly moved to the front of the pack globally.

The rise in research productivity for China’s biotech industry has caused Large Pharma to take note. Sanofi, Pfizer, Novartis and numerous others have made significant investments.

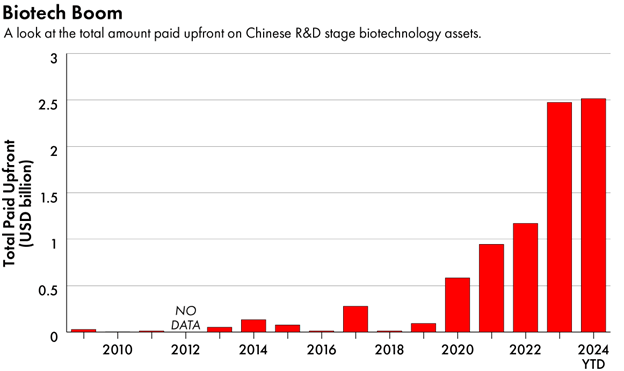

High R&D productivity has also yielded a relentless drumbeat of partnership announcements for assets licensed from Chinese biotechs to US biopharma and biotech companies.

Landmark deals such as Summit x Akeso’s PD-1 / VEGF bispecific antibody, Roche x Regor’s CDK2/4 inhibitor, and Merck x Lanova’s bispecific antibody, another entrant into the PD-1/VEGF space, demonstrate that Chinese biotechs are no longer relegated to ranks of producing only me-too and fast-follower assets. These are potential first-in-class medicines that could dominate multi-billion-dollar product categories for many years.

Source: DealForma. Graphic by The Wire China

Science Hubs Thriving in Shanghai and Suzhou

China biotech’s rise is one I have observed and needed to contend with firsthand. I serve as co-founder and CEO of a US precision oncology company, Meliora Therapeutics, based in Boston and San Francisco. We work on covalent allosteric small molecule drugs for breast cancer and other solid tumors.

Over the last 12-18 months, we started noticing that there seemed to be a Chinese competitor asset for every target we were exploring. M&A in the industry began slowing noticeably as Pharma buyers opted to license drug assets from China en masse – sometimes reaching multiple deals announced a week.

There were signs that we had reached a true tipping point in the industry in terms of R&D productivity and competitive landscape dynamics. We could no longer operate with the default assumption that US companies would be at the front of the pack.

To learn about what was actually happening on the ground, I spent time on the ground in Shanghai and Suzhou last month. I met many leading developers of small molecules, bispecific and trispecific antibodies, antibody-drug conjugates, and more. I toured their facilities.

What I saw would cause any biotech leader to sit up and take notice. I saw science parks many multiples larger than Kendall Square or South SF, filled with startups. Integrated biology, chemistry, biochem and structural biology, and vivarium labs were running at scale. Even smaller biotechs were running vivariums processing tens of thousands of in vivo mouse experiments monthly. Programs which went from standing start to registering for human clinical trials within 18 months(!) were not uncommon.

Speaking with the executives of local biotech leaders, I saw clinical development timelines which I estimate to be 50-100% faster than normal in the US or Europe. Depending on the novelty of the target, preclinical development timelines could be 100-200% faster than Western counterparts.

The proof on the ground was difficult to ignore. My experience raised the question whether the steady flow of business development news out of China may actually still be *understating* the accelerated R&D pace and novelty of China’s biopharma firms. The deals we have seen the past year could just be a preview of more to come.

What are the implications of this massive shift in the global biotech industry?

China’s rise sets a new standard for R&D productivity in terms of time and cost. This creates competitive pressure around the world. Generally speaking, capital will flow to areas of highest productivity. As asset IP development and R&D execution becomes cheaper, the premium for target selection and novel biology advantages increases.

This is true because Chinese biotechs, as fast as they are at execution, are often still limited in their understanding of the clinical and commercial value of different targets and programs in the Western market. This is understandable. Unless you have direct access to Western clinical key opinion leaders and understand the true treatment gap for patients in Western healthcare systems, being able to pick targets and target product molecule profiles is a very tall order.

Here is one place where US and European biotechs can continue to retain a comparative advantage.

Key point: In a world where R&D execution becomes ever more commoditized, novel scientific innovation is where the vast majority of the value creation in the therapeutics universe will accrue. American innovation should not cede its pole position.

How should American biopharma confront this change in the industry?

First, American biotechs should double down on its strengths in life sciences R&D. Exploring novel modalities of therapeutics to expand our drug toolkit, elucidating new underlying biological mechanisms to open up new therapeutic lines of attack against disease, and setting the global standard for converting translational / clinical trial insights into world class clinical patient care – these are the strengths US biotech must double down on as its unique advantages.

Second, American biotech should recognize the realities of our current situation and engage and partner with Chinese biotechs to leverage their strengths. In my opinion, the days of directly competing with Chinese biotechs in R&D execution are over for many (and perhaps soon, most) modalities of therapeutics.

Key point: Those who can pair best in world R&D execution with truly innovative and clinically meaningful biology hypotheses stand best positioned to garner capital, create more impactful medicines, and lead our industry.

What exactly does engaging and partnering with Chinese biotechs actually look like?

Here are a few directions US biopharma can take:

Ken Song, CEO, Candid Therapeutics

- License assets from Chinese partners after clinical de-risking in China (e.g. Summit x Akeso’s PD-1/VEGF bispecific antibody or ArriVent x Shanghai Allist’s EGFR inhibitor). Large pharma and numerous other groups are actively searching in this space, as it’s a fairly straightforward licensing structure. Future Chinese assets may not make it to late clinical stage before they are outlicensed to US / global firms.

- License preclinical or early clinical stage assets from a Chinese partner in order to help with clinical development. Candid Therapeutics is one example with multiple Chinese T-cell engager assets, and Hercules is another with multiple metabolic assets from Jiangsu Hengrui. In 2024, a number of these types of deals were announced as US venture capitalists began to explore earlier clinical stage pipelines from established Chinese biotech players. Aiolos Bio was one example of a company backed by US VCs with $245 million, with a TSLP-directed antibody from Jiangui Hengrui that was quickly acquired by GSK for more than $1 billion. (TR coverage). Interestingly, there are many more assets to comb through here in the China market.

- Form partnerships with China biotech companies to develop global IP for assets within a US umbrella newco. In this option, US firms can utilize their strengths in target discovery and target prioritization to guide the execution within a Chinese R&D organization and still retain IP rights outside China. However, execution is also difficult as close collaboration with Chinese biotech partners often requires on-the-ground presence and rare skills in navigating both US and China business culture.

Surely, all three types (and other derivatives) will continue to happen as the industry evolves, but the bottom line remains the same — successful biotechs, whether American, Chinese, or something else, will need to unlock true innovation. Gone are the days of me-too or fast follower plays. Technical and clinical innovation are the only ways forward.

There is a path for American biopharma to continue leading as the intellectual powerhouse of the industry — but that likely means leveraging the best R&D execution abilities wherever they are globally.

We owe it to American innovation to figure out what is that path. Patients, here and across the world, are waiting.

Investors, scientists, entrepreneurs, and policy makers interested in taking action on the significant opportunities ahead, feel free to message me on LinkedIn or X.com. I will also be at JPM conference in San Francisco.